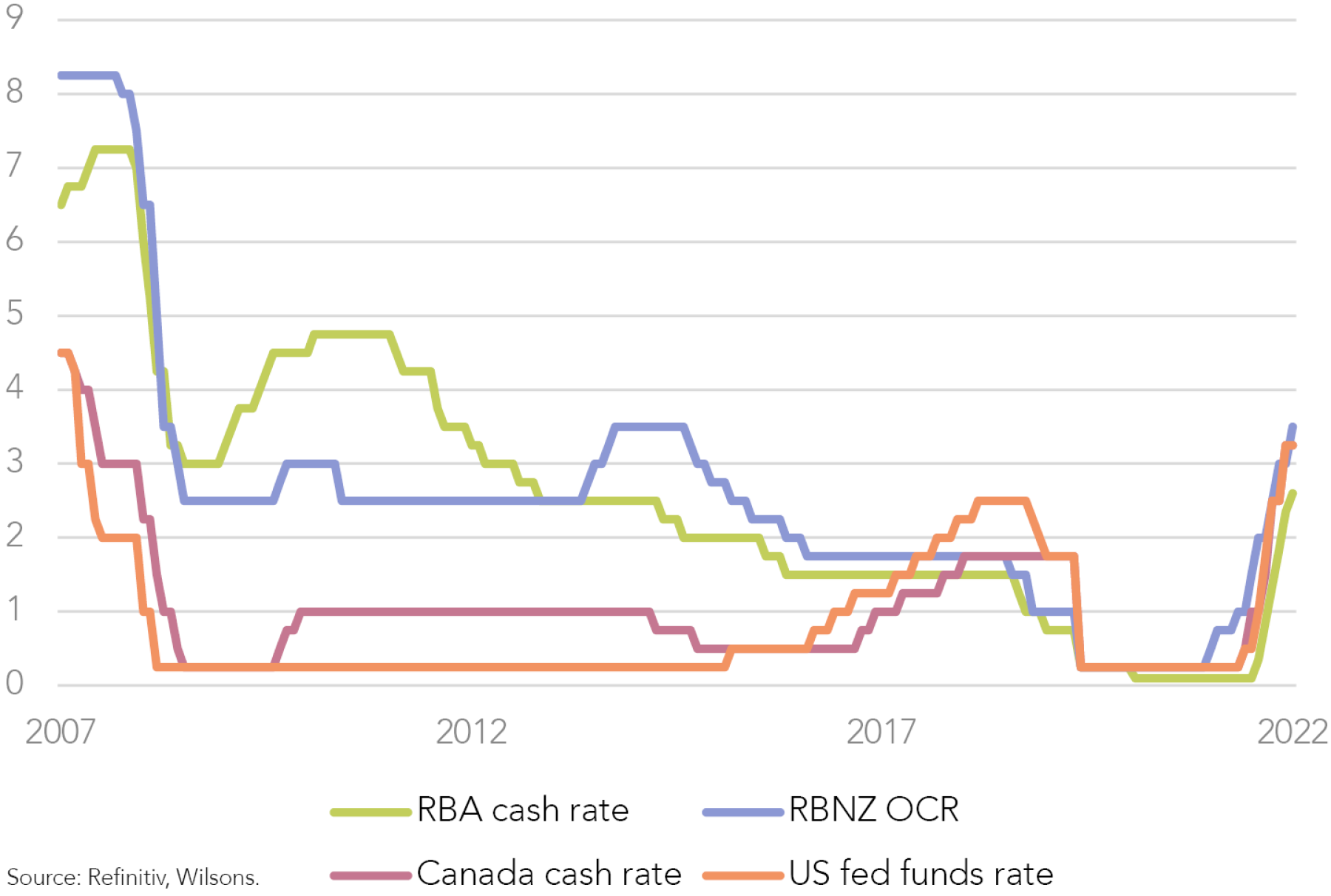

At its 4 October board meeting, the Reserve Bank of Australia (RBA) surprised the money market and economists alike with a lower than expected 25 basis point (bp) increase, taking the official cash rate to 2.6%.

The RBA had previously guided to a slowdown in the pace of rate hikes, although the consensus was still to expect one more 50bp hike before a step down to a 25bp increase at the November meeting.

The lower-than-anticipated rate increase might not seem like a huge shift in the grander scheme of things. Indeed, we still expect a 3.1% cash rate peak in December this year (previously November). However, the shift did have significant implications in terms of futures and bond market pricing. The (previously very hawkish) futures market shifted the assumed cash rate peak down from 4.1% to 3.6% (in mid-2023). Bond market yields fell in sympathy. (We note that futures market pricing at 3.6% is still above economists’ consensus peak.)

The RBA cited a few key factors in its decision to slow the pace of hiking. It highlighted that rates have moved a long way in a short space of time (250bps in 5 months). The RBA also highlighted that uncertainties around the global economy have grown. The RBA did, however, continue to signal that there is more work to do, stating, "further increases are likely to be required over the period ahead."

On balance, the market interpreted the October rate decision and policy statement as a “dovish pivot,” given the step down from 50 bp hikes to a 25bp move alongside relatively balanced commentary around the outlook. The RBA’s more dovish rhetoric stands in contrast to the currently hawkish posturing from most central banks, most notably the US Fed. At its late-September meeting, the Fed upgraded its guidance from its June cash rate guidance by 100 basis points to a peak cash rate of 4.6%.

While the Fed and RBA both have dual mandates of inflation control and full employment, the Fed is clearly prioritizing getting inflation back under control, and appears willing to risk a recession to do so.

In contrast, the RBA still seems focused on balancing inflation control against a desire to keep the economy growing at a decent pace.

Closer to home, the Reserve Bank of New Zealand (RBNZ) raised its cash rate by a more hawkish 50bp the day after the RBA. This takes the NZ cash rate to 3.5%.

Is a Less Aggressive Approach to Monetary Policy Prudent or Foolhardy?

So, why is the RBA taking a less hawkish attitude to monetary policy? Moreover, after its much-maligned guidance last year for rates to stay at zero until 2024, is the RBA now risking another overly dovish policy misstep? We think the RBA’s more tempered message on interest rates makes sense. There are a number of considerations that appear to support a more cautious approach to rate hikes from here.

Inflation pressures remain but with lower risk of a wage breakout

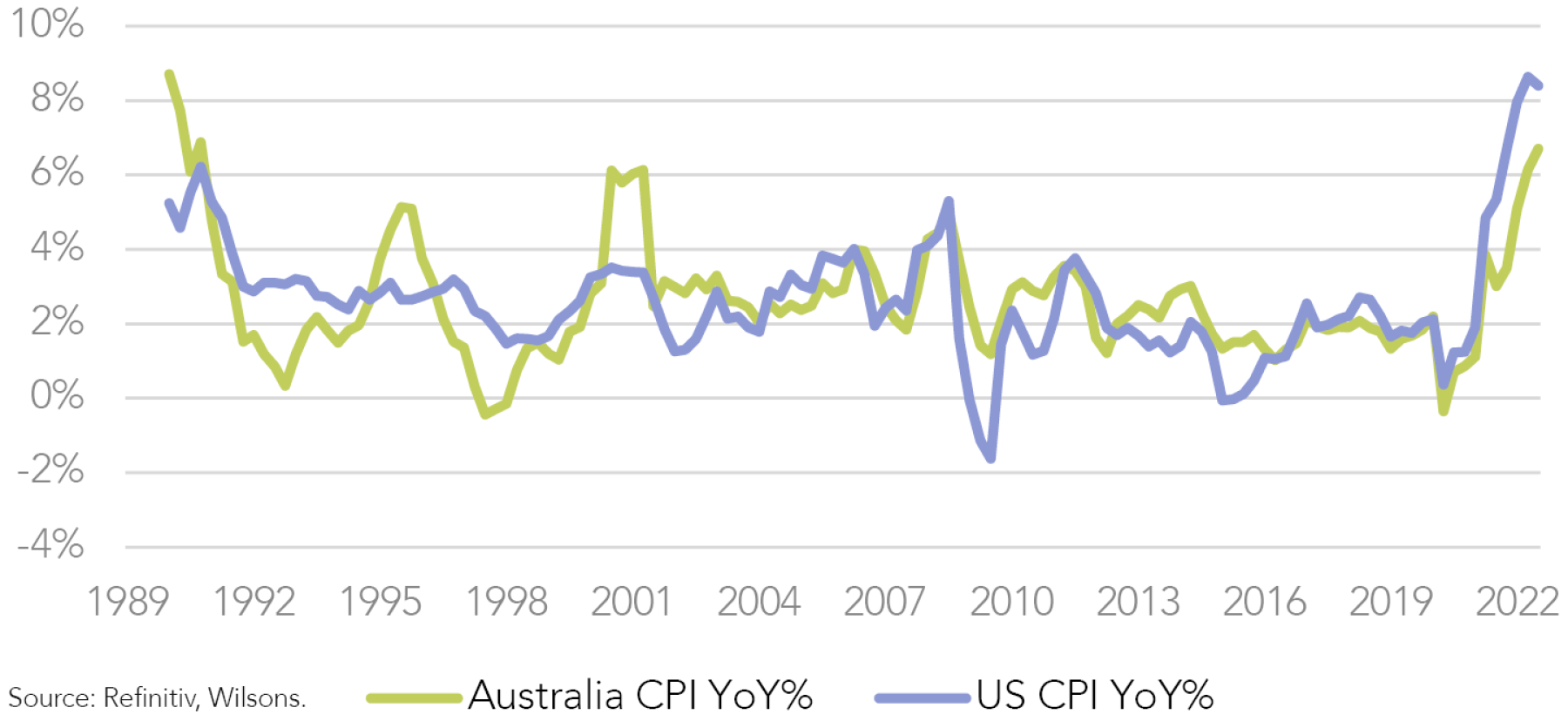

Australia is experiencing significant inflation pressures, much like the majority of western economies. However, Australian inflationary pressures do not appear quite as acute as in other economies. This is particularly the case on the wages front. Australian inflation pressures do appear to be lagging the US, with a peak likely in Q4 (likely October) at around 7.75% (RBA estimate). Wages are likely to lag even more given the institutionalised nature of our wage setting process and the quarterly release cycle of wage data. However, it is unlikely we will see wage growth (2.6% as June 30) push through 5% as it has in the US. The RBA has pointed out that while a strong domestic economy has played a role, a large part of inflationary pressure has come from global forces. Hence, there is a limit to what monetary policy can do. The RBA Governor has also called for responsible fiscal policy to help control inflation.

The RBA is aware of policy lags

The RBA would be acutely aware that monetary policy operates with a lag. This is the case even with our largely variable rate mortgage market (representing 80% of loans). Variable increases can take 1-2 months to filter through. Moreover, there has been a significant increase in fixed rate borrowing over the past 2 years. 40% of mortgages taken out in 2021 were 2-3-year fixed rate. Many of these fixed rate loans taken out in the second half of 2020 or in 2021 are set to expire over the coming year. As a result, the RBA’s policy-induced rate shock has yet to hit many households. From this perspective, the RBA is likely to pause soon and wait to see how its initial rate rises impact Australians over the first half of 2023.

Australian households are very highly geared

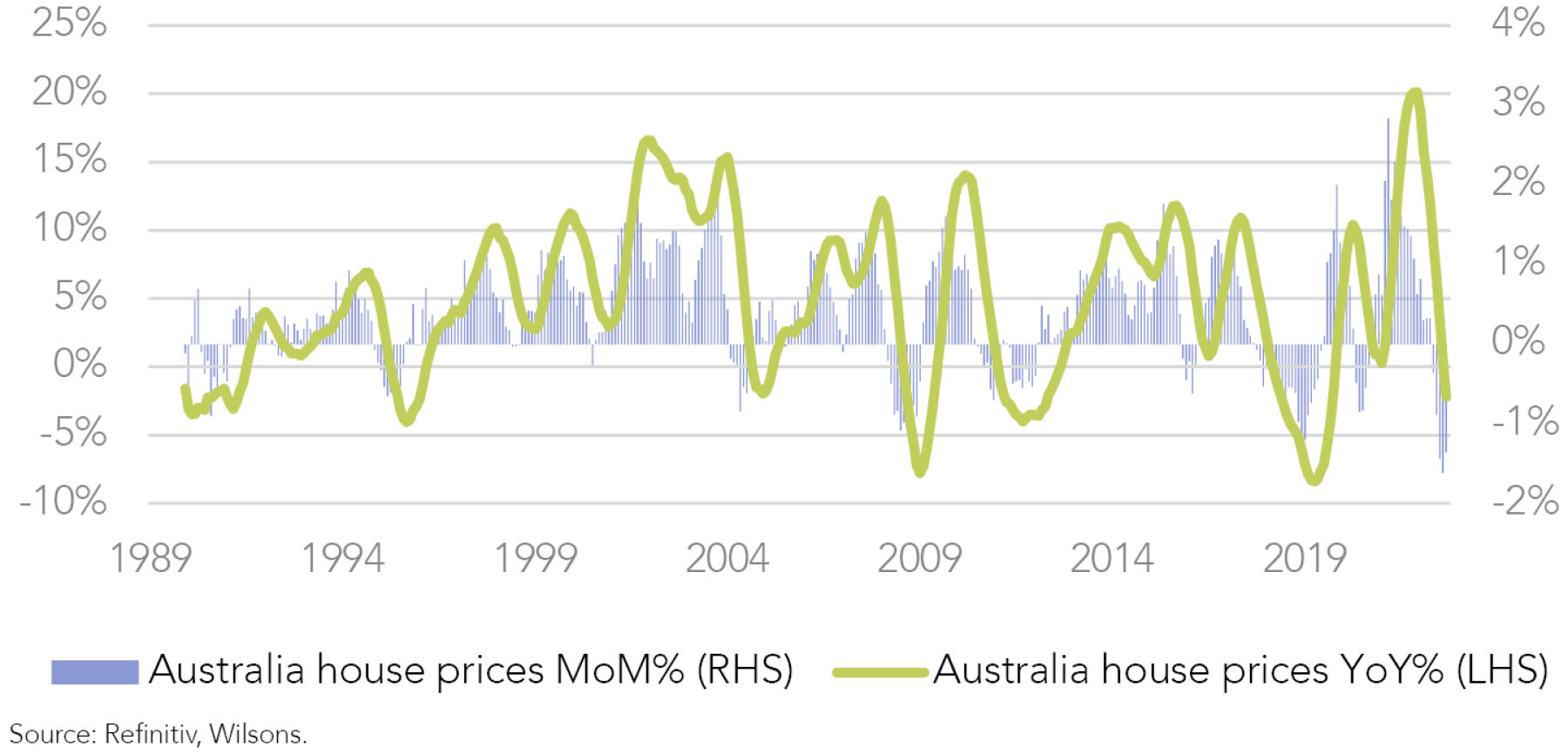

Australian households are also more highly geared, with our household debt-to-income ratio almost twice that of the US. This high gearing, combined with the variable rate bias of the mortgage market, makes Australia very sensitive to shifts in the cash rate. From this perspective, it makes sense that the RBA is becoming more circumspect on rate rises. While the economy itself has shown resilience to rate rises so far, house prices are now down 5.8% from their peak, which coincided with the start of the tightening cycle. The RBA would be aware that the risk of a dangerous house price unwind in Australia (greater than 20% decline) is relatively high. In addition, while the average mortgage holder is well ahead (22 months) on their mortgage payments, borrowers who have committed to a mortgage over the last couple of years would have a limited buffer, and are likely sitting right on the cusp of a significant shift in disposable income. 25% of households have a buffer of less than 2 months.

While mortgages are meant to be stress tested for 250-300bp (APRA) of hikes – which is about what we expect the RBA will do – there are likely to be some households who find themselves

over-geared. At a minimum, many households will face a significant drop in disposable income over the coming year, crimping their spending.

The RBA Partial Pivot Appears Prudent

In summary, the RBA pivot appears prudent given the lags involved in monetary policy impact and the high level of gearing in the Australian economy. There is some risk that the RBA may be dragged into more tightening next year (as the futures market still suggests), although our base case is that as we approach the peak cash rate (3.1%), that should slow the economy significantly next year. We see the risk of recession as low relative to other economies given our more circumspect central bank and our currently strong economic momentum.

This is a “relative” positive for our share market and our bond market. A lower peak cash rate is likely to drag on the AU$, though we believe the biggest swing factors for the AU$ are: (1) whether the Fed pauses by year end (and when the market seriously contemplates a Fed cutting cycle); and( 2) the general “risk-on” or “risk-off” nature of financial markets over the coming year. The A$ is a “risk-on” currency. We continue to see long-term fair value in the low 70s at least. On that basis, we see some partial hedging of foreign exposures as worthwhile.

Written by

David Cassidy, Head of Investment Strategy

David is one of Australia’s leading investment strategists.

About Wilsons Advisory: Wilsons Advisory is a financial advisory firm focused on delivering strategic and investment advice for people with ambition – whether they be a private investor, corporate, fund manager or global institution. Its client-first, whole of firm approach allows Wilsons Advisory to partner with clients for the long-term and provide the wide range of financial and advisory services they may require throughout their financial future. Wilsons Advisory is staff-owned and has offices across Australia.

Disclaimer: This communication has been prepared by Wilsons Advisory and Stockbroking Limited (ACN 010 529 665; AFSL 238375) and/or Wilsons Corporate Finance Limited (ACN 057 547 323; AFSL 238383) (collectively “Wilsons Advisory”). It is being supplied to you solely for your information and no action should be taken on the basis of or in reliance on this communication. To the extent that any information prepared by Wilsons Advisory contains a financial product advice, it is general advice only and has been prepared by Wilsons Advisory without reference to your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of your own objectives, financial situation and needs before following or relying on the advice. You should also obtain a copy of, and consider, any relevant disclosure document before making any decision to acquire or dispose of a financial product. Wilsons Advisory's Financial Services Guide is available at wilsonsadvisory.com.au/disclosures.

All investments carry risk. Different investment strategies can carry different levels of risk, depending on the assets that make up that strategy. The value of investments and the level of returns will vary. Future returns may differ from past returns and past performance is not a reliable guide to future performance. On that basis, any advice should not be relied on to make any investment decisions without first consulting with your financial adviser. If you do not currently have an adviser, please contact us and we would be happy to connect you with a Wilsons Advisory representative.

To the extent that any specific documents or products are referred to, please also ensure that you obtain the relevant disclosure documents such as Product Disclosure Statement(s), Prospectus(es) and Investment Program(s) before considering any related investments.

Wilsons Advisory and their associates may have received and may continue to receive fees from any company or companies referred to in this communication (the “Companies”) in relation to corporate advisory, underwriting or other professional investment services. Please see relevant Wilsons Advisory disclosures at www.wilsonsadvisory.com.au/disclosures.