In the course of this reporting season, we have yet to witness any major reporting disasters, and overall the data has been relatively positive.

Currently, 45% of companies on the S&P/ASX 200 have reported their financial results, representing more than half of the benchmark on a market capitalisation basis. According to the results reported, 37% of companies had earnings beats of over 2%, and 27% had earnings misses of more than -2%. We believe this paints a positive picture of Australian earnings' resilience in FY22.

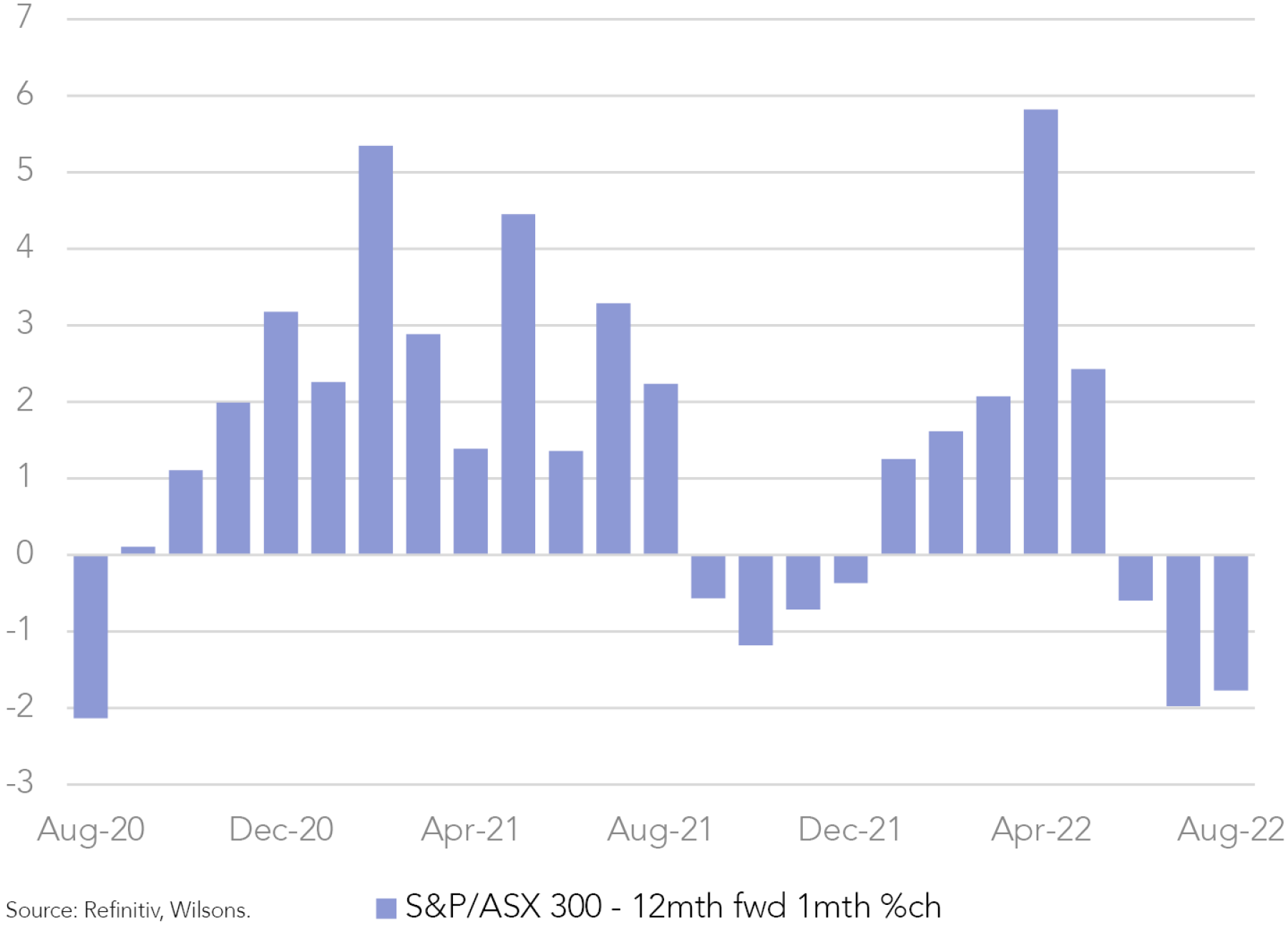

We believe the most suitable gauge of performance in a reporting season tends to be 12-month forward earnings revisions. Although we are still seeing downgrades at an index level, they are occurring at a slower pace than they were prior to reporting.

Once we remove commodity-oriented sectors like materials, energy and utilities, earnings revisions have been flat on average. Currently, we think this reporting season is on course for a pass mark. Therefore, so far, so good.

| Name | Ticker | Sector | 12mth fwd EPS (1 Month Revision) |

| Medibank Private Ltd | MPL | Financials | 9% |

| COMPUTERSHARE LIMITED | CPU | Information Technology | 7% |

| QBE Insurance Group Ltd | QBE | Financials | 6% |

| Brambles Ltd | BXB | Industrials | 5% |

| Commonwealth Bank of Australia | CBA | Financials | 3% |

| Suncorp Group Ltd | SUN | Financials | 3% |

| Insurance Australia Group Ltd | IAG | Financials | 3% |

| Seek Ltd | SEK | Communication Services | 2% |

| Vicinity Centres | VCX | Real Estate | 2% |

| JB Hi-Fi Ltd | JBH | Consumer Discretionary | 2% |

| Telstra Corporation Ltd | TLS | Communication Services | 1% |

| Santos Ltd | STO | Energy | 1% |

| Goodman Group | GMG | Real Estate | 1% |

| Carsales.Com Ltd | CAR | Communication Services | 1% |

| Dexus | DXS | Real Estate | 1% |

| Orora Ltd | ORA | Materials | 0% |

| Treasury Wine Estates Ltd | TWE | Consumer Staples | 0% |

| AMP Ltd | AMP | Financials | 0% |

| BHP Group Ltd | BHP | Materials | 0% |

| Steadfast Group Ltd | SDF | Financials | 0% |

| Endeavour Group Ltd | EDV | Consumer Staples | 0% |

| Cochlear Ltd | COH | Health Care | 0% |

| Evolution Mining Ltd | EVN | Materials | -1% |

| ASX Ltd | ASX | Financials | -1% |

| Amcor PLC | AMC | Materials | -1% |

| GPT Group | GPT | Real Estate | -1% |

| Bendigo and Adelaide Bank Ltd | BEN | Financials | -1% |

| Challenger Ltd | CGF | Financials | -2% |

| Mirvac Group | MGR | Real Estate | -2% |

| Rio Tinto Ltd | RIO | Materials | -3% |

| James Hardie Industries PLC | JHX | Materials | -3% |

| CSL Ltd | CSL | Health Care | -3% |

| Resmed Inc | RMD | Health Care | -3% |

| REA Group Ltd | REA | Communication Services | -3% |

| Aurizon Holdings Ltd | AZJ | Industrials | -5% |

| Downer EDI Ltd | DOW | Industrials | -6% |

| Stockland Corporation Ltd | SGP | Real Estate | -7% |

| BlueScope Steel Ltd | BSL | Materials | -8% |

| Newcrest Mining Ltd | NCM | Materials | -9% |

| AGL Energy Ltd | AGL | Utilities | -12% |

| Origin Energy Ltd | ORG | Utilities | -13% |

| Fisher & Paykel Healthcare Corporation Ltd | FPH | Health Care | -15% |

*as at 22/08/2022

Source: Refinitiv, Wilsons.

Consumer Pain not there (yet)

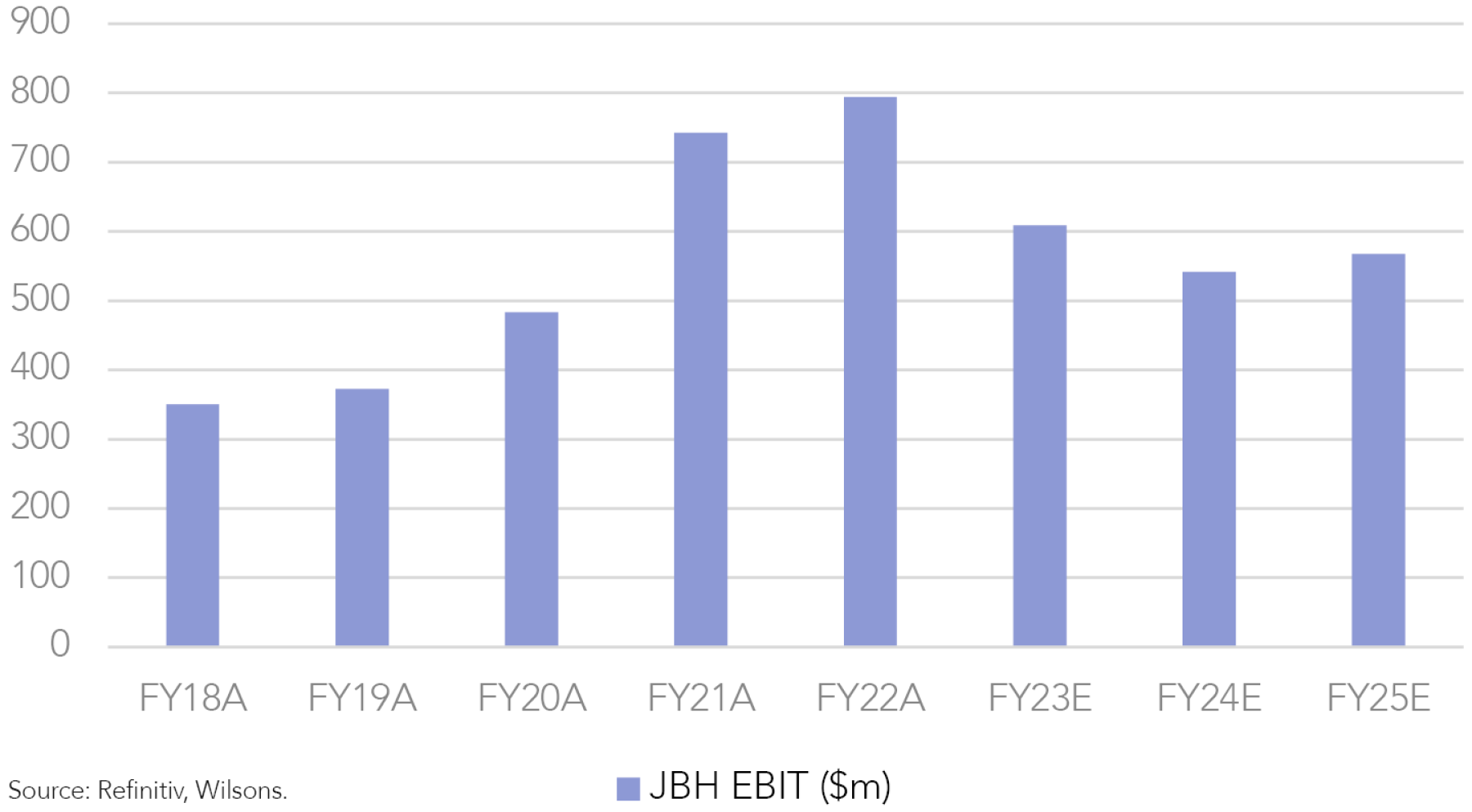

JB Hi-Fi (JBH) had an impressive result and showed signs that, even with rising interest rates and low levels of consumer sentiment, the Australian consumer was still willing to go out and spend on electronics up to the end of June.

We thought the earnings call had some interesting snippets. Firstly, Terry Smart (CEO) agreed that gross margins would start to compress over the next 12 months as they see more on-floor discounting. We believe this shows management expect demand to fade in FY23.

Secondly, the CEO also discussed how the products they sell are less discretionary than they used to be. The CEO gave the example of how mobile phones have become “very much integrated into our customers’ lives”. Although there is an element of truth to this, we still think that when push comes to shove, consumers will cut back on the next gadget to pay their bills, and we remain sceptical that this type of spending will hold up in an economic slowdown.

Although FY22 performance was above expectations, we do not think the results call painted any overly bullish picture for earnings in FY23.

Financials Upgraded

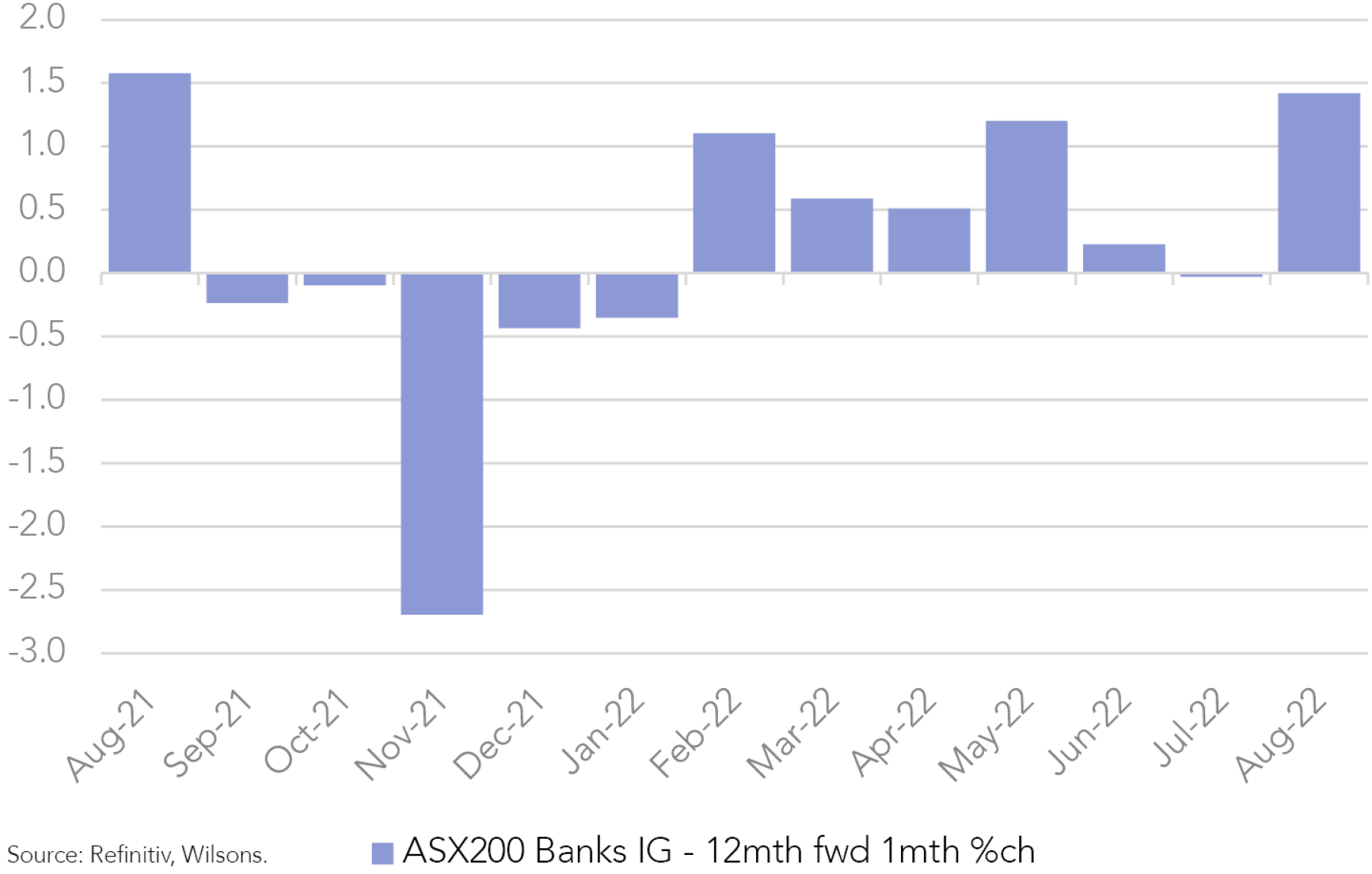

The insurance and banking sectors have also seen earnings upgrades this reporting season.

Commonwealth Bank of Australia's (CBA) FY22 results were mostly in line with market expectations, but we found the discussion on net interest margins (NIMs) particularly interesting. The bank expects to see margins increase as interest rates rise since it passes more of the Reserve Bank's (RBA) interest rate rises onto borrowers than savers. Similarly, National Australia Bank (NAB) predicted that NIMs would increase in FY23.

CBA discussed the impact of cost pressures. As a result of higher wages, CBA's costs increased 8% half on half. In the second half of this calendar year, the big 4 banks may face more cost headwinds. Our expectation is that any potential cost increases over the next 6 months will be offset by NIM growth. Overall, the market has been upgrading the big 4 banks in August.

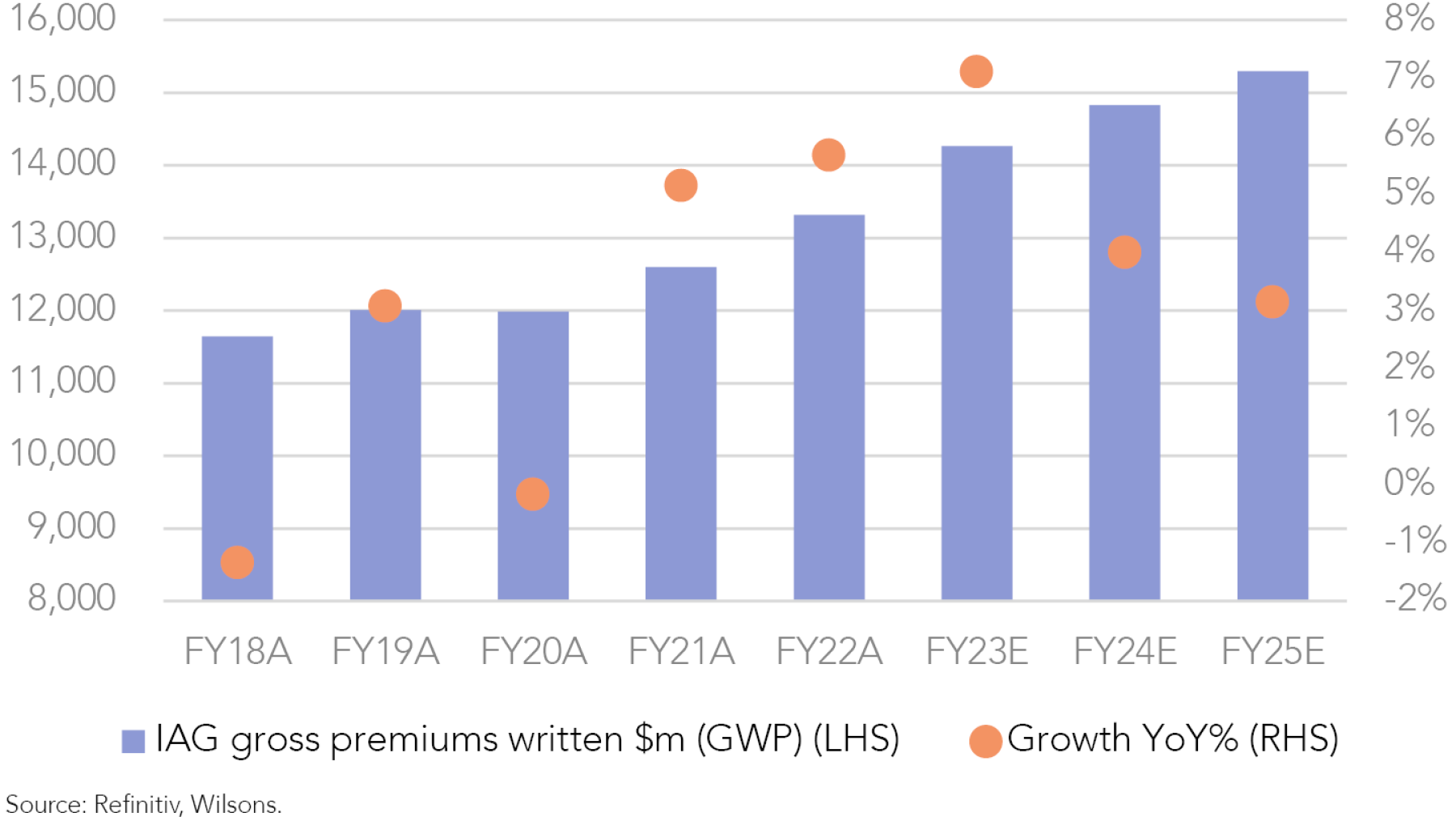

Through August, insurance companies have also seen upgrades. Insurance Australia Group’s (IAG) full-year results highlighted that premiums will likely rise in the year ahead, following sharp rises in the year to June. We have seen this trend across many insurers, from NIB Group to QBE Group. The current macro environment appears to be beneficial for insurers.

Online Classifieds Speeding along

Seek (SEK) and Carsales (CAR) surprised the market with large jumps in revenue and profits from a surge in advertising in the jobs and car markets. These figures were above market expectations, providing signs that the economy was in relatively good shape going into June.

In both earnings calls, management provided strong outlooks, albeit with significant caveats.

Carsales’ CEO stated that they expected to see “very strong growth” in revenue in FY23 and confirmed that auto-market conditions remained buoyant.

Seek confirmed guidance for FY23 that was above market expectations for revenue and earnings before interest, taxes, depreciation and amortization (EBITDA). The market did not seem to react well to the CEO’s comments on assumptions around guidance, where he stated, “We have assumed a low risk of job market volatility from monetary policy, geopolitical change and the pandemic. If this assumption changes, revenue could fall below guidance”

REA Group (REA) reported an earnings miss, but the share price was up 6.7% on the day (one of the best ASX 100 daily share price moves so far). We think this was a relief rally to counter investor expectations that property listings would be very weak in the fourth quarter of FY22 - but were actually less weak than expected. This is proof that overly-bearish (or overly-bullish) market positioning can lead to surprising share price outcomes on the day of a result.

While we are somewhat cautious on the outlook for housing, jobs and autos, these are high quality businesses where, over the medium-term, the structural story should outweigh the cyclicality.

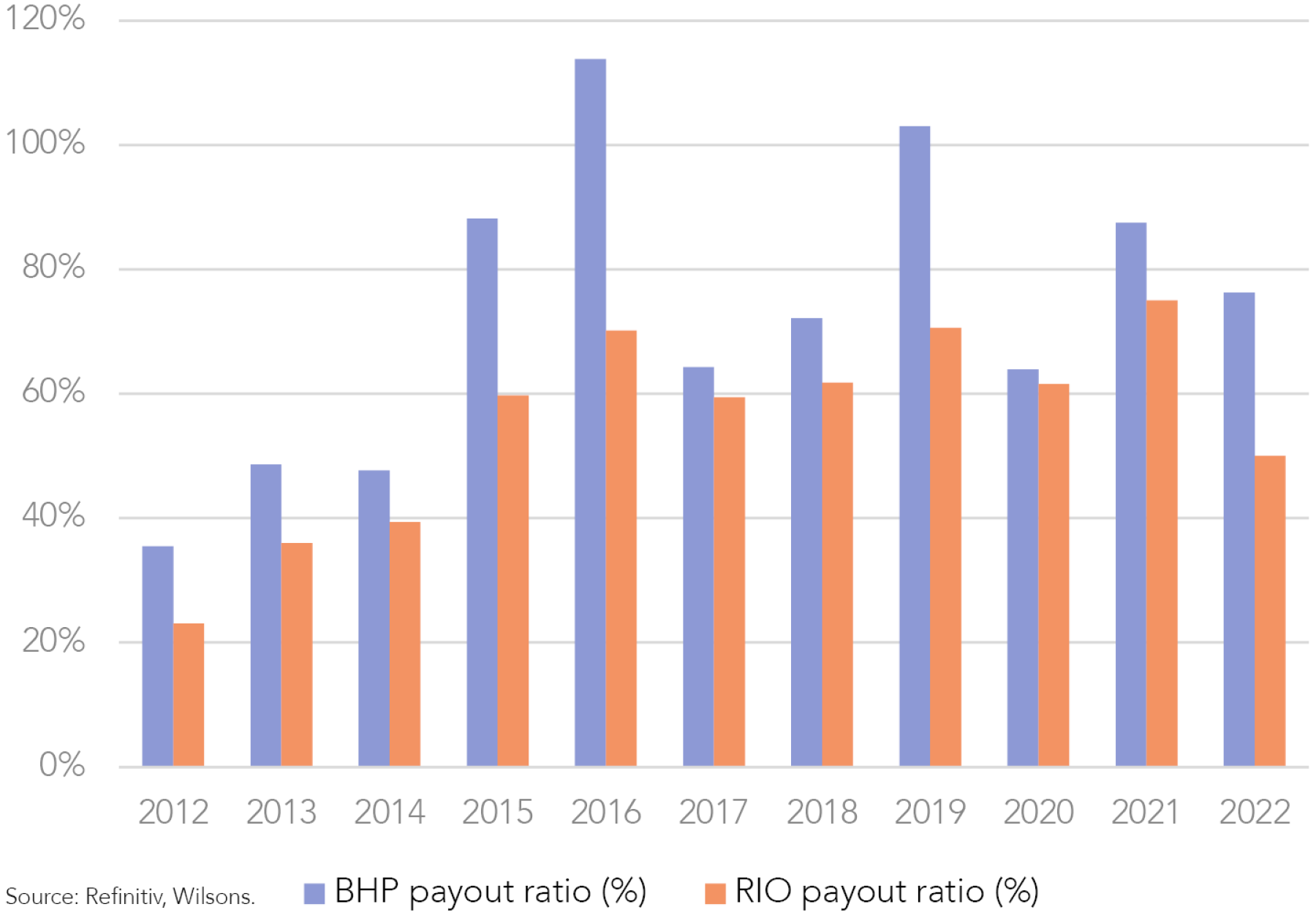

Dividend Outlook Mixed for Major Miners

Updates from the major iron ore miners to date have reaffirmed our preference towards BHP Group (BHP) over Rio Tinto (RIO) and Fortescue Metals (FMG).

From a capital management perspective, BHP announced that it would return US$36b to shareholders in FY22 (including the in-specie dividend of US$19b from the BHP Petroleum divestment to Woodside (WDS)). Dividend per share (DPS) was US$3.25 for full-year FY22, which was consistent with expectations and reflected a payout ratio of 77% (vs 89% pcp).

In contrast, RIO disappointed investors as it lowered its payout ratio and returned less capital to investors than expected in its June half result. RIO will pay an interim ordinary dividend of US$4.3b or US$2.67 per share, reflecting a reduced payout ratio of ~50% (down from ~75% pcp).

RIO’s management has flagged a more challenging market environment given commodity market headwinds and widespread operating cost inflation. For BHP, we think these risks are partially mitigated by its more diversified asset portfolio, which has a growing exposure to ‘green’ metals like nickel and copper.

BHP was up 4.1% on the day, likely another relief rally on the expectation of a below-consensus result on the dividend. After a poor RIO result, the market potentially expected more of the same from BHP.

Investment Implications

Underweight consumer goods

As we stated when the RBA started to raise interest rates, we want to avoid sectors that will likely see demand erosion due to cost-of-living pressures. Consumer goods like electronics are still areas of the market we are trying to avoid over the short-term. We prefer service companies like Aristocrat (ALL), Lotteries Corp (TLC) and Qantas (QAN), which should benefit from pent-up demand for these services after COVID restrictions.

Economy strong in FY22 but expect some weakness in FY23

We think there is evidence in earnings reports of management concern on the economic outlook so far.

Financials starting to show resilience

Banks and insurance companies are beginning to show their quality at offsetting inflation and rates pressures. We remain neutral on the banks but overweight on insurance.

Dividends (and earnings) now peaked for major miners

We think earnings and dividends have peaked for major miners like BHP and RIO and remain underweight the sector, with a preference to BHP.

| Company | Ticker | Date | Event | EPS actual (cps, reported currency) | EPS expected (consensus) (cps, reported currency) | % Surprise vs Consensus | Comments |

| Pinnacle Investment Management Group | PNI | 3/08/2022 | FY22 Results | 39.5 | 39.4 | 0.30% | Understandably, the result was impacted by market volatility (transitory/style underperformance), especially in 4Q22a (FUM -$7.7b net) and softer than expected affiliate margins. Looking forward, flows remain net positive and affiliate margins should benefit from recent mandate wins and eventually growth investment. |

| Telstra | TLS | 11/08/2022 | FY22 Results | 14.4 | 14 | 2.90% | In-year NBN headwinds of $340m - marking the end of the NBN headwinds with a cumulative EBITDA impact of $3.6bn p.a. FY23 guidance is for EBITDA of $7.8-8.0bn vs prior ambition of $7.5-8.0bn and vs consensus of $7.8bn. Positive momentum was evident in the key mobile division, which drove a +700m EBITDA increase underpinned by 155K net adds and ARPU growth of +2.9%. TLS also reaffirmed its commitment to realizing the value of its infrastructure assets, with InfraCo Fixed mooted as the next division to be monetized. Overall the result supports our positive view of TLS. |

| IAG | IAG | 12/08/2022 | FY22 Results | 8.5 | 11.1 | -23.40% | As expected, earnings was relatively uneventful with key numbers being pre reported. NPAT was $347m inline with expectations, driven by gross written premium (GWP) growth of 5.7%. Result was negatively impacted by higher net peril costs (~$1.1b) and reserve strengthening. IAG reaffirmed FY23 guidance for GWP growth in the mid to high single digits range and for insurance margins of 14-16%. We remain positive on IAG and expect GWP growth to outpace claims inflation and support margins in FY23. |

| Healthco Healthcare and Wellness REIT | HCW | 12/08/2022 | FY22 Results | 5.1 | 5 | 2.70% | The result was underpinned by strong operating performance with 100% rent collections and 99% portfolio occupancy at the end of the period. HCW provided FY23 guidance of FFO of 6.8 cps (+10% YoY) and DPU of 7.5cps (flat YoY). From a capital management perspective, HCW announced an on-market unit buyback (specific details are yet to be provided) and highlighted the importance of redeploying capital into value accretive investment opportunities including the committed development pipeline. |

| Resmed | RMD | 12/08/2022 | FY22 Results | 579 | 573 | 1.00% | ResMed’s 4Q22 result was a beat vs consensus and was in line with Wilsons estimates (non-GAAP EPS US$1.49/share) and showed early evidence that the card-to-cloud ‘stop-gap’ (C2C) is leading renewed CPAP share gains in USA. Management confirmed that C2C sales were material in the quarter. ROW progress looked slower notwithstanding new jurisdictional AS11 launches. Wilsons analysts' new FY23e forecast has ResMed capturing US$285M of the US$600M Philips ‘hole’ that is ostensibly available over the next year while the business is sidelined from the market due to its product recall. |

| News Corp | NWS | 15/08/2022 | 4Q22 Trading Update | 120 | 90 | 33.30% | Adjusted EPS was US120cps in FY22, above expectations of US90 cps. The key digital real estate services segment, which includes REA Group, grew revenue +25% over the year to US$.17bn despite cycling tough comps. Segment EBITDA grew by +12% to US$574m as it was impacted by one-off costs. The outlook for FY23 depends largely on the macro backdrop. Supply chain and cost pressures are expected to persist over the next year. Visibility on the ad market remains limited across the business. We remain favourable towards NWS and continue to see a hidden value in the group that can be unlocked as progress is made on its simplification strategy. |

| Seek | SEK | 16/08/2022 | FY22 Results | 7.29 | 7.09 | 2.90% | EBITDA of $509m vs consensus of $512m in FY22. FY23 EBITDA guidance of $560-$590m vs consensus of $550m. Management stated that the macro environment creates downside revenue risks. However, SEK can reduce discretionary costs as it has done before to limit impact. Overall, a strong result and guidance supports our investment thesis on SEK. Cyclical factors (i.e. a strong jobs market) have been a key driver of supernormal growth over the last year, but we still think the digitalisation of ads is a strong structural driver for SEK’s business over the medium term (especially in Asia). |

| BHP Group | BHP | 16/08/2022 | FY22 Results | 421 | 407 | 3.40% | Result inline with our expectations. In our view, we have now probably seen peak earnings for BHP as we expect softer iron ore prices over the next 6-12 months; lead by an improvement in supply from Brazil and lower demand from China. DPS inline with consensus at US$3.25. EBITDA of US$40.6bn line with consensus. The payout ratio of 77% led to a DPS of US$3.25, inline with market expectations. This was contrary to RIO, which lowered its payout ratio to 50% and returned less than expected in 1H22. |

| James Hardie | JHX | 16/08/2022 | 1Q23 Trading Update | 35 | 36 | -2.80% | Net income increased +15% pcp to US$154m, below consensus of US$162m. Disappointingly , FY23 guidance was lowered -3.2% at the mid-point to US$730m-US$780m from the prior range of US$740-US$820m. The downgrade was driven by a weakening macro backdrop. Notwithstanding price increases, higher input and freight costs have squeezed margins and a softening in housing markets has created uncertainty around the demand for construction materials globally. |

| Goodman Group | GMG | 16/08/2022 | FY22 Results | 81.3 | 81.7 | -0.50% | Strong result as we expected. Operating EPS grew +24% pcp to 81.3 cps in FY22, above guidance of +23% (previously upgraded from +10% and +20%) and broadly inline with consensus. DPS was unchanged at 30 cps as expected. FY23 guidance is or operating EPS of 90.3 cps (+11% pcp) above consensus forecasts of 89.8 cps. Overall, the result reaffirms our positive view towards GMG, which we expect to keep benefiting from positive operating conditions over the long-term term. We think continued growth in GMG’s funds management operations is positive as the market typically pays a premium for annuity style earnings. |

| Santos | STO | 17/08/2022 | 1H22 Results | 38 | 34 | 12.00% | Underlying profit US$1,267m, slightly above consensus ($1,131m). US$605m in shareholder return, implies a payout ratio of 35% of FCF. Overall, a positive result with an earnings beat, however, we were hoping to see a higher payout ratio than 35%. We continue to believe STO is behind the curve on capital management relative to global peers |

| CSL | CSL | 17/08/2022 | FY22 Results | 480 | 485 | -1.00% | Wilsons analysts assess underlying FY22 profit of US$2,185M after omitting a US$70M benefit from non-recurring COVID vaccine manufacturing contract (AstraZeneca) and Vifor acquisition transaction costs. NPAT was towards the top end of management's guidance range. Positively, FY23 constant currency guidance (NPAT US$2.4-2.5B, ex-Vifor) was 5% ahead of estimates by Wilsons Research and implies 10%-14% growth versus FY22. |

| Telix Pharmaceuticals | TLX | 18/08/2022 | 1H22 Results | na | na | na | Telix reported a 1H22 loss of $70M which was higher than the market modelled. Although consistent with previously reported cash flows the update may have dashed some hopes elsewhere across the market of an FY23e profit debut (WILSe:FY24e). Telix provided some encouraging colour with respect to its ILLUCCIX launch, recording US$9.1M sales in July (the first month with reimbursement support in USA). Telix closed 1H22 with $122M cash and no debt. At this stage Wilsons analysts are reasonably comfortable that the group can achieve sustainable profitability by FY24E without further recourse to equity financing. |

| Cleanaway Waste Management Ltd | CWY | 19/08/2022 | FY22 Results | 6.9 | 7.2 | -4.20% | Result broadly in line. U/L EBITDA increased +8.7% pcp to $582m, above consensus of $572m. FY23 outlook for EBITDA (excl GRL contributions) of $630-670m ($650 mid-point) looks a little soft compared consensus of $667m. Separately, CWY also announced that it will acquire 100% of Global Renewables Holdings (GRL) for $168.5m at an FY22A EV/EBITDA multiple of 7.9x. The business will raise $350m via a fully underwritten institutional placement and up to $50m via a non-underwritten retail purchase plan. We view this as a savvy acquisition that future proofs the business (recycling the future, in our view), is EPS accretive (~3.7% on a FY22A pro forma basis) and scales up the business further. |

Source: Refinitiv, Wilsons.

Written by

David Cassidy, Head of Investment Strategy

David is one of Australia’s leading investment strategists.

About Wilsons Advisory: Wilsons Advisory is a financial advisory firm focused on delivering strategic and investment advice for people with ambition – whether they be a private investor, corporate, fund manager or global institution. Its client-first, whole of firm approach allows Wilsons Advisory to partner with clients for the long-term and provide the wide range of financial and advisory services they may require throughout their financial future. Wilsons Advisory is staff-owned and has offices across Australia.

Disclaimer: This communication has been prepared by Wilsons Advisory and Stockbroking Limited (ACN 010 529 665; AFSL 238375) and/or Wilsons Corporate Finance Limited (ACN 057 547 323; AFSL 238383) (collectively “Wilsons Advisory”). It is being supplied to you solely for your information and no action should be taken on the basis of or in reliance on this communication. To the extent that any information prepared by Wilsons Advisory contains a financial product advice, it is general advice only and has been prepared by Wilsons Advisory without reference to your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of your own objectives, financial situation and needs before following or relying on the advice. You should also obtain a copy of, and consider, any relevant disclosure document before making any decision to acquire or dispose of a financial product. Wilsons Advisory's Financial Services Guide is available at wilsonsadvisory.com.au/disclosures.

All investments carry risk. Different investment strategies can carry different levels of risk, depending on the assets that make up that strategy. The value of investments and the level of returns will vary. Future returns may differ from past returns and past performance is not a reliable guide to future performance. On that basis, any advice should not be relied on to make any investment decisions without first consulting with your financial adviser. If you do not currently have an adviser, please contact us and we would be happy to connect you with a Wilsons Advisory representative.

To the extent that any specific documents or products are referred to, please also ensure that you obtain the relevant disclosure documents such as Product Disclosure Statement(s), Prospectus(es) and Investment Program(s) before considering any related investments.

Wilsons Advisory and their associates may have received and may continue to receive fees from any company or companies referred to in this communication (the “Companies”) in relation to corporate advisory, underwriting or other professional investment services. Please see relevant Wilsons Advisory disclosures at www.wilsonsadvisory.com.au/disclosures.