Since the beginning of the year, the Focus List has been underweight iron ore miners. We continue to believe the fundamentals for iron ore (and the miners that produce it) are skewed to the downside over the medium-term.

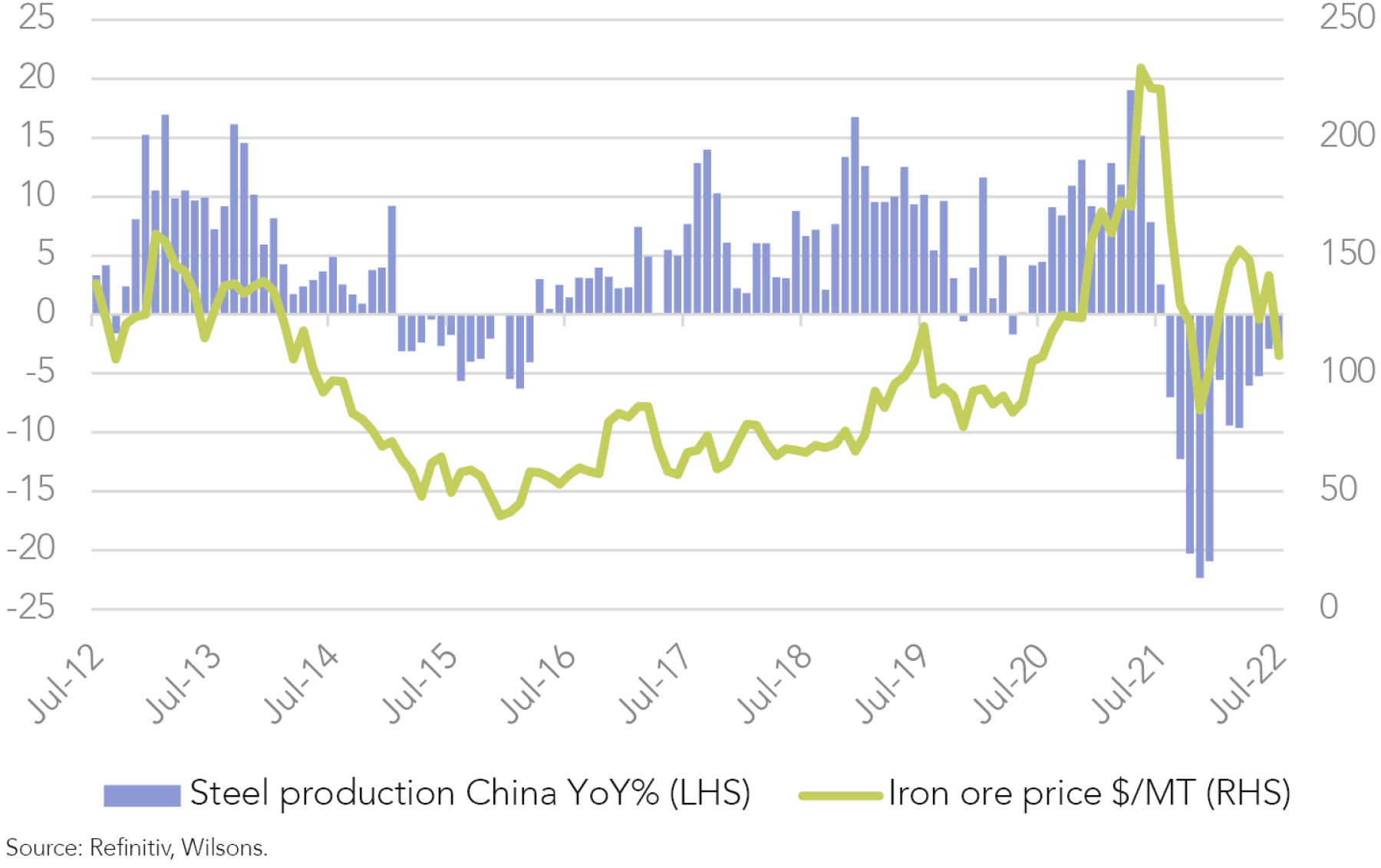

Currently, it looks less likely Chinese demand will bounce back after a COVID-impacted first half. We do not discount China's capacity to provide more stimulus to the economy, which would likely boost steel production and, therefore, iron ore prices.

The mixed demand picture comes alongside new supply, which continues to come online from major producers in Australia, as well as an expected recovery in Brazilian supply for the rest of this year following recent weather-related weakness.

Demand Revival Fading

During the first half of the year, there was optimism that Beijing's support for the property and infrastructure sectors would boost steel production. This moved the price to ~US$150/MT in April 22.

Over the past 3-6 months, China's zero-COVID policy has posed a significant headwind. Since March, there have been several new COVID-19 outbreaks and related containment measures across many Chinese provinces, which prevented any stimulus from materially impacting the economy and, more importantly for iron ore, supporting the demand for steel.

China’s zero-COVID policy is still inflicting further strains on the economic outlook. This week, several Chinese cities, including Haikou on the southern island of Hainan, as well as Urumqi in the western Xinjiang region, have imposed or extended lockdown restrictions in some areas, with cases rising nationwide over the weekend.

China will likely introduce more stimulus over the course of this year but combined with a zero-case policy, we think it will likely be insufficient to support steel demand. We don't believe China will abandon its zero-COVID policy anytime soon.

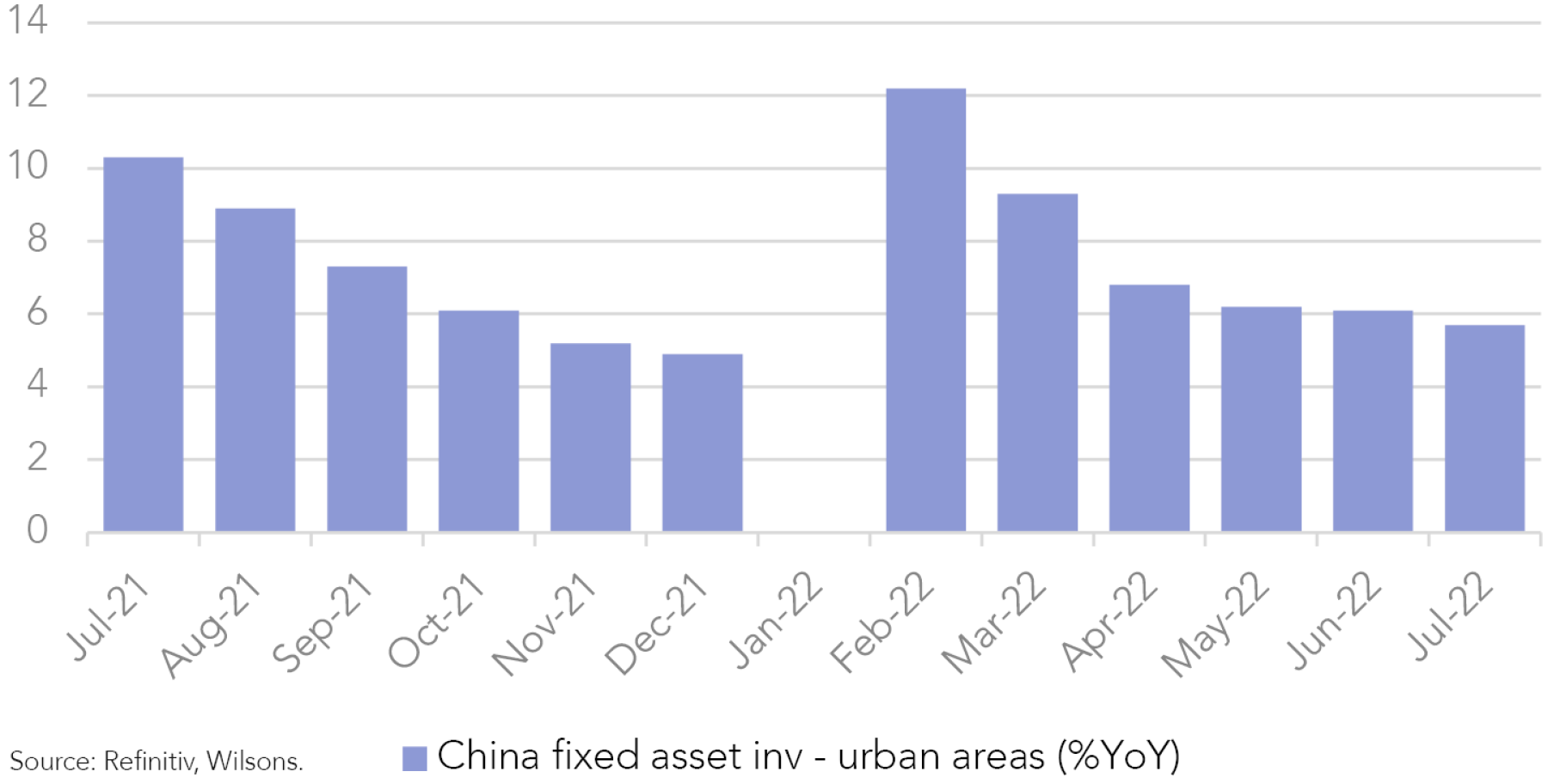

The zero-COVID policy has exacerbated a property market already under stress, with developers (such as Evergrande) under significant financial pressure and investors losing faith in the market. This has been evident in the economic data. Construction of property, which typically accounts for about 40% of China's steel end-use demand, has slowed in H122, falling by 34%. Recent July data indicated a deceleration across production, investment and consumption under the crushing weight of the zero-COVID policy.

Stimulus not to be discounted

A key risk to our view is that Beijing could implement a material stimulus package this calendar year that provides meaningful support for iron ore.

Despite our belief that China's property and financial markets will likely improve over the next year, we believe this will occur at a time when supply starts to ramp up and the level of stimulus may underwhelm.

Supply recovering

Weather disruptions appear to have affected Brazilian production in the early part of this year, with heavy rains in Vale’s Southern and South-Eastern systems, as well as CSN’s Casa de Pedra mine. This has been a tailwind for price as the market has remained tight.

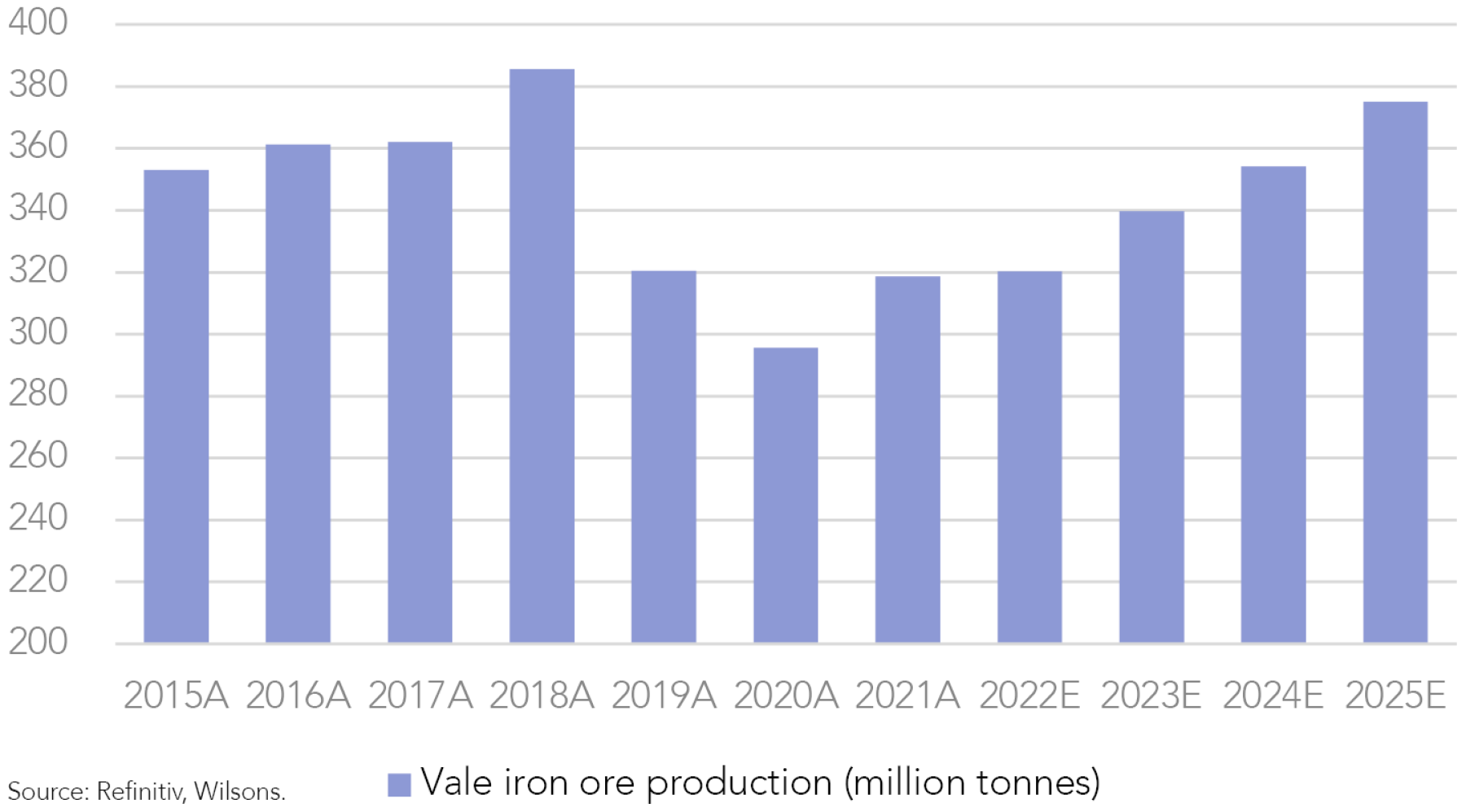

However, we believe Brazilian supply is likely to recover throughout the rest of the year following the recent weakness. Brazil’s largest producer, Vale, had a total production of 74 million tonnes in the June quarter 2022, 17% higher quarter-on-quarter.

For 2022, Vale has guidance at 310 to 320 million tonnes, and while there is an element of seasonality to production, this would still imply a very strong second half as the miner only produced 137 million tonnes in the first half.

According to estimates, Brazilian exports will reach 373 million tonnes in 2022, up 4.5% from 2021. By 2024, Brazil's total iron ore exports are predicted to grow by around 5.8% annually, reaching around 420 million tonnes.

Australian exports are also expected to grow from 894 million tonnes in 2022 to 948 million tonnes in 2024. We believe this should be a significant headwind to iron ore prices over the medium-term as China’s demand starts to stagnate.

Iron ore prices remain vulnerable to supply shocks in 2022

May saw record rainfall in the Pilbara due to severe weather. A negative phase of the Indian Ocean Dipole - which tends to bring more rainfall to northern Australia - could cause further disruptions to production and exports in coming months.

A third La Niña for next (southern hemisphere) summer could also be another headwind for Brazilian supply. Further heavy rains would likely negatively impact Vale’s mines as they did in 2021-22.

In recent months, Australian producers have also reported ongoing labour supply shortages, both in existing operations and in bringing new production capacity online.

| Spot (16/08/22) | CY22 | CY23 | CY24 | Long Term | |

| Iron Ore Price (US$/t) | 113 | 135 | 121 | 101 | 75 |

Source: Refinitiv, Wilsons.

Focus List Remains Underweight Iron Ore Miners

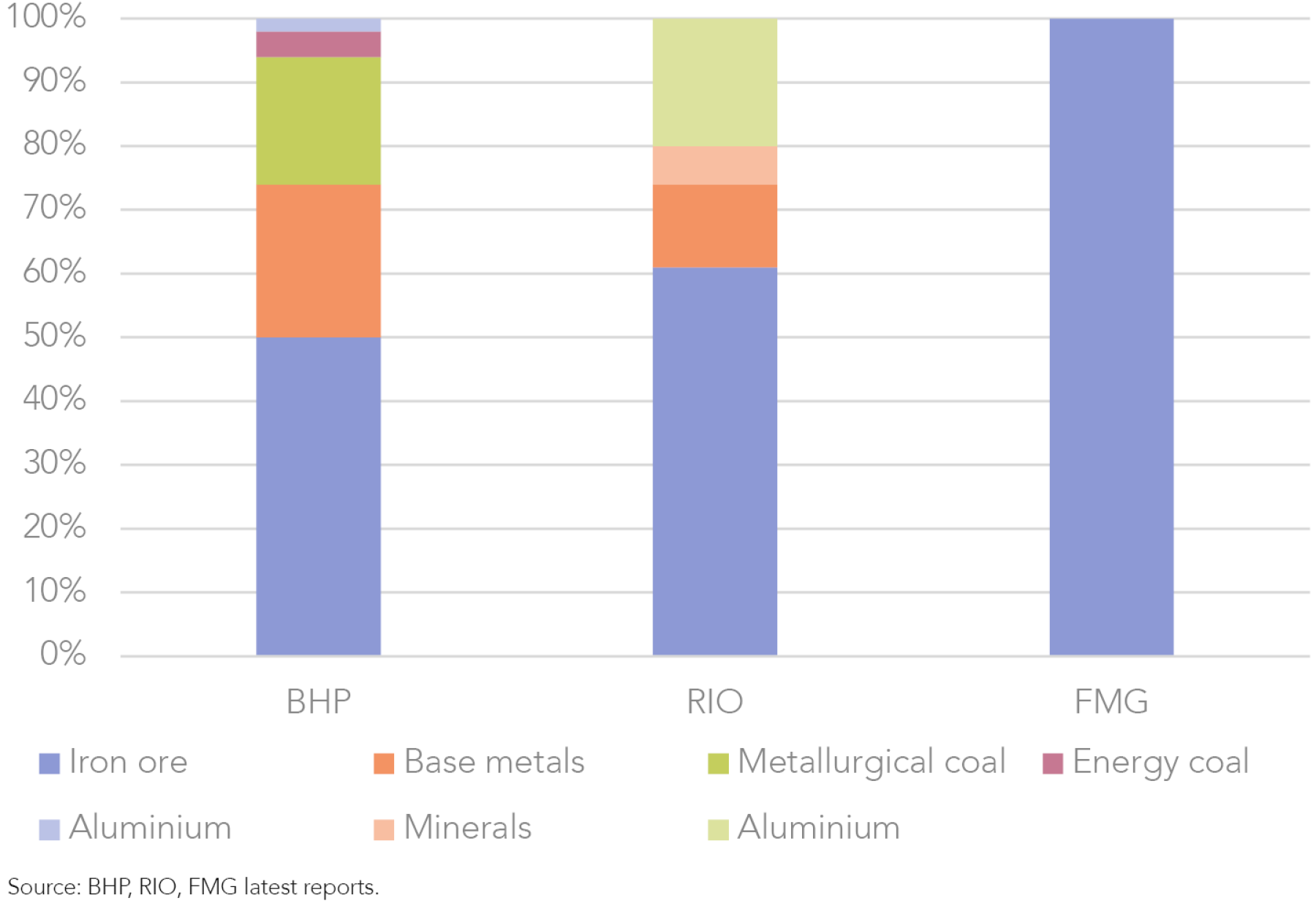

We are underweight iron ore miners in the Focus List at an 8% weighting in BHP Group Ltd (BHP). Approximately 12-13% of the ASX 200 is composed of the three major iron ore producers: BHP, Rio Tinto (RIO) and Fortescue Metals Group (FMG). We remain underweight in the sector due to our more bearish view on iron ore.

BHP is our pick of the major players

The miner has a large, low cost, tier 1 asset portfolio that is more diversified than the other major players with a smaller concentration towards iron ore.

We believe that BHP’s strategy towards EV minerals is astute and removes some of the ESG issues of its past (thermal coal and oil).

RIO still has too many operational risks. We believe BHP has less operational risks at present relative to RIO.

Diversification and transition

BHP and RIO, unlike FMG, have a diversified commodity mix. We believe this is important to hedge against any downside risk in iron ore.

In our view, BHP has been effectively managed over the years and we are supportive of its current strategy. BHP’s goal is to maximize the value of its core iron ore and metallurgical coal (steel-making coal) assets while also increasing exposure to 'future-facing' commodities including EV minerals like copper and nickel, where the company already has the largest and second largest resource endowments globally.

BHP’s recent (rejected) takeover bid for ASX listed copper/nickel player OZ Minerals (OZL) is evidence of this strategy. We think BHP’s measured approach towards primarily copper and nickel is sound given the clear operational synergies with its existing iron ore business.

In contrast, we view RIO’s push into lithium extraction and processing, and FMG’s investments into new and unproven green hydrogen technologies as less complementary to their core operations. We therefore view these as fraught with integration risks.

More ESG friendly

BHP has also been phasing out from its non-core fossil-fuel assets, including the spinoff of BHP Petroleum (oil and gas) to Woodside Petroleum (now Woodside Energy) in June 2022, the sale of its 80% stake in BHP Mitsui Coal (thermal coal) to Stanmore Resources (SMR) in May 2022, and the sale of Cerrejón (thermal coal) to Glencore In January 2022.

We think this has given BHP a tick from an ESG perspective. Over time we anticipate BHP will become an increasingly diversified miner with a greater focus on ‘green’ commodities that are likely to be in structural deficits for some time.

Risks remain in RIO

- RIO has had poor operational performance in core iron ore operations resulting in multiple cuts to guidance.

- ESG – RIO has no coal exposure but we have concerns on governance after the Juukan Gorge incident.

- Capital discipline is less clear with a recent pivot towards growth.

- Mongolian Oyu Tolgoi project is high risk (block cave) – CapEx overruns and start-up delays result in high in-price.

FY23e EBITDA |

|||

| BHP | RIO* | FMG | |

| US$80/t | -33% | -32% | -47% |

| US$100/t | -18% | -12% | -20% |

| Spot | -9% | 1% | -7% |

*RIO is a Dec YE. BHP and FMG are June.

Source: Refinitiv, Wilsons.

| FCF Yield FY23 (Consensus) |

FCF Yield (at LT prices) |

Div. Yield FY23 (Consensus) |

Div. Yield (at LT prices) |

EV/EBITDA FY23 (Consensus) |

EV/EBITDA (at LT prices) |

|

| BHP | 9% | 2% | 9% | 2% | 4.5 | 10.6 |

| RIO | 6% | 2% | 9% | 2% | 3.9 | 10.6 |

| FMG | 9% | -5% | 9% | 1% | 4.9 | 17.2 |

*LT price at consensus US$75/t.

Source: Refinitiv, Wilsons.

Written by

David Cassidy, Head of Investment Strategy

David is one of Australia’s leading investment strategists.

About Wilsons Advisory: Wilsons Advisory is a financial advisory firm focused on delivering strategic and investment advice for people with ambition – whether they be a private investor, corporate, fund manager or global institution. Its client-first, whole of firm approach allows Wilsons Advisory to partner with clients for the long-term and provide the wide range of financial and advisory services they may require throughout their financial future. Wilsons Advisory is staff-owned and has offices across Australia.

Disclaimer: This communication has been prepared by Wilsons Advisory and Stockbroking Limited (ACN 010 529 665; AFSL 238375) and/or Wilsons Corporate Finance Limited (ACN 057 547 323; AFSL 238383) (collectively “Wilsons Advisory”). It is being supplied to you solely for your information and no action should be taken on the basis of or in reliance on this communication. To the extent that any information prepared by Wilsons Advisory contains a financial product advice, it is general advice only and has been prepared by Wilsons Advisory without reference to your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of your own objectives, financial situation and needs before following or relying on the advice. You should also obtain a copy of, and consider, any relevant disclosure document before making any decision to acquire or dispose of a financial product. Wilsons Advisory's Financial Services Guide is available at wilsonsadvisory.com.au/disclosures.

All investments carry risk. Different investment strategies can carry different levels of risk, depending on the assets that make up that strategy. The value of investments and the level of returns will vary. Future returns may differ from past returns and past performance is not a reliable guide to future performance. On that basis, any advice should not be relied on to make any investment decisions without first consulting with your financial adviser. If you do not currently have an adviser, please contact us and we would be happy to connect you with a Wilsons Advisory representative.

To the extent that any specific documents or products are referred to, please also ensure that you obtain the relevant disclosure documents such as Product Disclosure Statement(s), Prospectus(es) and Investment Program(s) before considering any related investments.

Wilsons Advisory and their associates may have received and may continue to receive fees from any company or companies referred to in this communication (the “Companies”) in relation to corporate advisory, underwriting or other professional investment services. Please see relevant Wilsons Advisory disclosures at www.wilsonsadvisory.com.au/disclosures.